Global Logistics Market Outlook 2032

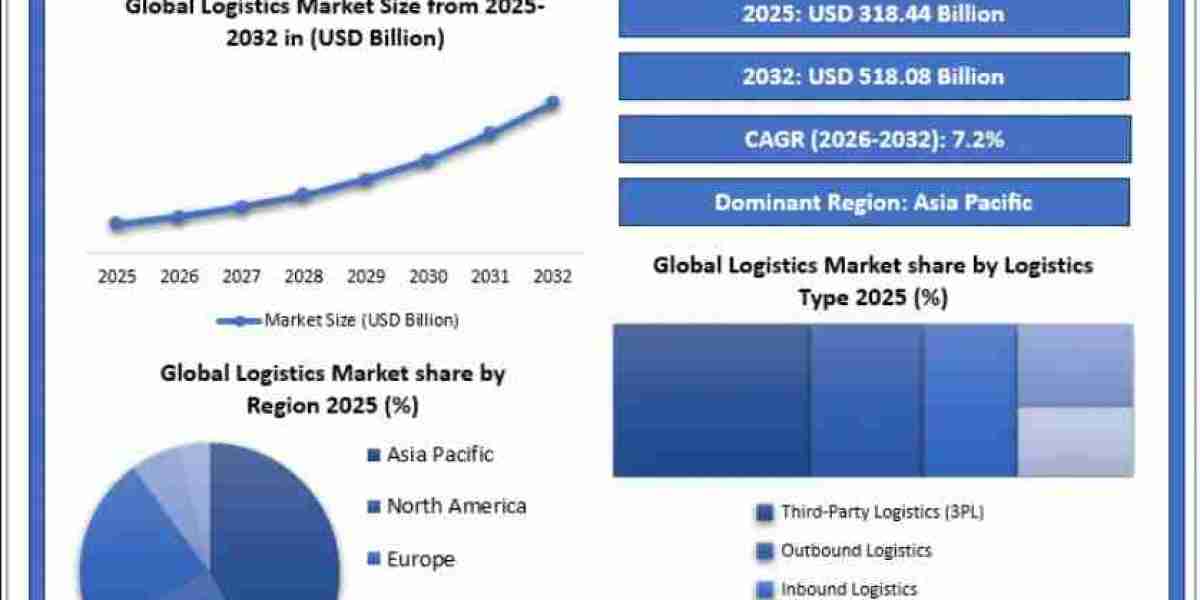

The global Logistics Market is entering a transformative growth phase, fueled by the rapid expansion of e-commerce, digital supply chain technologies, automation, and smart transportation networks. The market is projected to grow from USD 318.44 billion in 2025 to nearly USD 518.08 billion by 2032, registering a CAGR of 7.2% during the forecast period. As global trade networks become increasingly interconnected, logistics providers are focusing on speed, efficiency, sustainability, and real-time visibility to meet evolving customer expectations.

The logistics industry has evolved far beyond traditional freight movement and warehousing. Today, it plays a central role in enabling digital commerce, supporting industrial supply chains, and improving cross-border trade operations. Companies are integrating artificial intelligence, IoT-enabled tracking systems, cloud logistics platforms, robotics, and predictive analytics to optimize transportation routes, improve delivery accuracy, and reduce operational costs.

To know about the Research Methodology :- Request Free Sample Report@https://www.maximizemarketresearch.com/request-sample/94795/

Rising E-Commerce Demand Accelerating Logistics Expansion

One of the strongest drivers shaping the logistics market is the extraordinary growth of global e-commerce. Online retail sales increased from approximately USD 4.98 trillion in 2021 to nearly USD 6.86 trillion in 2025, and are expected to exceed USD 8 trillion by 2027. This sharp rise in online shopping has significantly increased the demand for warehousing, transportation, fulfilment centers, and last-mile delivery services.

The growing number of digital consumers has also intensified the need for faster and more reliable delivery systems. Consumers now expect same-day or next-day delivery services, particularly in urban areas. As a result, logistics companies are investing heavily in regional distribution hubs, micro-fulfilment centers, and automated sorting facilities to reduce delivery times and improve customer satisfaction.

The expansion of cross-border e-commerce is further strengthening the logistics sector. Businesses are increasingly relying on third-party logistics providers (3PLs) and integrated supply chain partners to manage international shipping, customs documentation, inventory management, and reverse logistics operations efficiently.

Technology Transforming the Logistics Ecosystem

Digital transformation is becoming the foundation of modern logistics operations. Logistics providers worldwide are adopting advanced technologies to improve visibility, operational control, and transportation efficiency.

IoT-enabled tracking systems are helping companies monitor cargo movement in real time, improving shipment transparency and reducing losses. Around 48% of logistics firms in advanced economies are already utilizing IoT tracking technologies for predictive delivery management and smart freight monitoring.

Artificial intelligence is also revolutionizing logistics planning. AI-powered analytics tools are being used for route optimization, warehouse forecasting, fuel efficiency management, and predictive maintenance. These solutions enable companies to reduce delays, optimize resource utilization, and improve supply chain resilience.

Warehouse automation is another major growth area within the logistics market. Robotics and automated material handling systems are improving warehouse productivity and reducing dependency on manual labor. Nearly 53% of logistics firms across OECD economies have implemented robotics in warehouse operations to improve shipment handling efficiency and inventory accuracy.

Cloud-based logistics platforms are also gaining widespread adoption. These systems allow logistics companies, suppliers, retailers, and transportation providers to collaborate through centralized digital networks, ensuring seamless coordination across global supply chains.

Last-Mile Delivery Becoming a Competitive Advantage

Consumer preference for faster deliveries is reshaping the structure of logistics networks worldwide. Last-mile delivery has emerged as one of the most critical and competitive segments in the industry. Urban logistics providers are under constant pressure to deliver packages more quickly while minimizing transportation costs and environmental impact.

Average urban delivery times have improved significantly, decreasing from 2.36 days in 2022 to 2.15 days in 2023. This improvement is largely driven by investments in localized fulfilment centers, route optimization software, AI-driven scheduling systems, and automated delivery infrastructure.

At the same time, rising parcel volumes are creating additional operational challenges. China currently leads global parcel activity with more than 900 million parcels annually, followed by the United States with 500 million parcels and Germany with around 400 million parcels. Such massive shipment volumes are encouraging logistics companies to invest in scalable infrastructure and advanced automation technologies.

Sustainability and Green Logistics Gaining Importance

Environmental sustainability is becoming a major focus area for the logistics industry. Increasing urban congestion, rising fuel costs, and stricter environmental regulations are pushing logistics providers to adopt greener transportation solutions.

Companies are introducing electric delivery vehicles, low-emission freight transportation systems, and energy-efficient warehouses to reduce carbon emissions. Green logistics initiatives are also encouraging the use of multimodal transportation networks that combine rail, waterways, and road transport to optimize fuel efficiency.

Several leading logistics providers have already begun large-scale sustainability investments. Electric heavy-duty trucks, AI-based fuel optimization systems, and carbon-neutral warehousing projects are becoming important differentiators in the global market.

To know about the Research Methodology :- Request Free Sample Report@https://www.maximizemarketresearch.com/request-sample/94795/

Asia Pacific Dominates the Global Logistics Market

Asia Pacific continues to dominate the global logistics landscape due to rapid industrialization, expanding manufacturing activity, and booming e-commerce adoption. Countries such as China, India, Japan, and Southeast Asian economies are witnessing strong demand for transportation, warehousing, and fulfilment services.

The region handles more than 1.8 billion e-commerce parcels annually, making it the largest logistics hub globally. China remains the world’s largest logistics and manufacturing center, while India is emerging as a high-growth market supported by digital commerce, infrastructure investments, and government-led supply chain modernization initiatives.

North America and Europe also maintain strong positions in the logistics market due to advanced transportation infrastructure, high automation adoption, and strong cross-border trade activities. These regions are increasingly focusing on smart logistics solutions, warehouse robotics, and sustainable transportation systems to maintain competitiveness.

Challenges Limiting Market Growth

Despite strong growth potential, the logistics industry faces several operational and financial challenges. Rising transportation and fuel costs remain major concerns for logistics operators worldwide. Freight transportation accounts for a substantial share of total logistics expenditure, especially in developing economies.

Labor shortages, infrastructure bottlenecks, supply chain disruptions, and fluctuating fuel prices continue to impact delivery efficiency and operational profitability. Air freight costs remain significantly higher compared to rail and water transport, making cost optimization a key priority for logistics companies.

Additionally, increasing pressure to meet sustainability targets requires continuous investments in green technologies, fleet modernization, and energy-efficient logistics infrastructure.

Competitive Landscape

The global logistics market remains highly competitive, with major international players focusing on digital transformation, automation, and strategic expansion initiatives. Leading companies are strengthening their global networks through acquisitions, warehouse expansions, AI integration, and multimodal transportation capabilities.

Major companies operating in the market include DHL Group, Kuehne + Nagel, DSV A/S, DB Schenker, CEVA Logistics, A.P. Moller – Maersk, UPS Supply Chain Solutions, Sinotrans Limited, Lineage Logistics, and Americold Logistics.

Regional logistics companies such as Delhivery, Blue Dart Express, Mahindra Logistics, and Allcargo Logistics are also expanding rapidly through technology adoption and e-commerce partnerships.

Future Outlook

The future of the global logistics market will be shaped by automation, artificial intelligence, sustainable transportation, and digitally connected supply chains. As consumer expectations continue to evolve, logistics providers will increasingly prioritize speed, transparency, flexibility, and environmental responsibility.

The integration of AI-powered analytics, IoT-enabled tracking, autonomous warehousing systems, and cloud logistics platforms is expected to redefine global logistics operations over the next decade. Companies that successfully combine operational efficiency with sustainable and technology-driven logistics solutions are likely to gain a strong competitive advantage in the rapidly evolving global market.